One of the easiest mistakes in investing is to believe that because markets have risen for a while, they will continue to rise.

They won’t.

Not because the world is ending. Not because anybody rang a bell at the top. Simply because that’s how markets behave.

Over the long term, shares have been one of the most rewarding assets an investor can own. But the journey has never been smooth.

Roughly one year in every four delivers a negative return.

That’s not a flaw.It’s the admission price.

After several years of strong growth, it’s perfectly reasonable to expect that at some point we’ll experience a pullback. Nobody knows whether that’s next month, next year or further down the road. What we do know is that eventually it will happen.

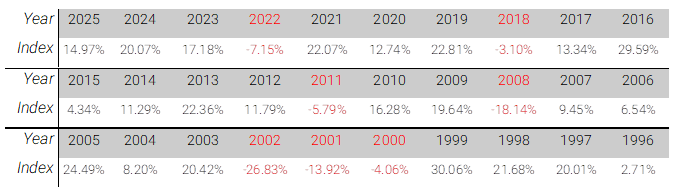

In over thirty years of advising clients, I’ve seen the same pattern repeat itself countless times. Markets rise, confidence grows, headlines become optimistic and investors start to believe that this time might somehow be different. Then, often without warning, markets remind us that setbacks are normal. Look at the table below.

This table provides the annualised past performance of global stock markets (equities) as measured by the FTSE World Index, which is a market-capitalisation weighted index representing the performance of large-and mid-cap stocks from the FTSE Global Equity Index Series and covers 95% of the investable market capitalisation. It covers Developed and Advanced Emerging markets.

The successful investors aren’t the ones who predict these moments.

They’re the ones who prepare for them.

And that’s exactly why we build a plan.

When markets fall, our response should not be panic. Nor should it be surprise.

The response should be: “This is what we planned for.”

The plan was never designed for the easy years. Anyone can feel clever when markets rise. The real test comes when headlines become frightening and emotions become expensive.

Staying the course during those periods isn’t doing nothing.

It’s executing the plan.

There is, however, one area where I believe investors should be uncompromising.

Money that you expect to spend over the next five years should not be exposed to stock market risk.

If you’re drawing income from your portfolio, helping children onto the housing ladder, funding a major purchase, or simply planning to supplement your lifestyle, that money needs a different job description.

Its purpose isn’t growth.

Its purpose is certainty.

The reason is simple.

Imagine markets fall by 25% at precisely the moment you need to withdraw money. You’re forced to sell investments when prices are depressed. Even if markets recover later, part of your portfolio has already been sold and can no longer participate in that recovery.

The impact can last far longer than the market decline itself.

This is why we separate short-term spending from long-term investing.

The first pot is the Liquidity Pot.

This holds cash and short-dated fixed income designed to fund spending over the next few years – typically five. Its job isn’t excitement. Its job is reliability. It allows you to meet your spending needs without worrying about what the stock market happens to be doing this month.

The second pot is the Longevity Pot.

This is invested for the future. It owns the growth assets that have historically built wealth over long periods. Because it isn’t needed immediately, it can be given the time required to recover from the inevitable setbacks that markets occasionally deliver.

Think of it as keeping enough fuel in the tank before setting off on a long journey. You don’t spend the whole trip staring anxiously at the fuel gauge when you know you’ve prepared properly.

This isn’t a strategy for nervous investors. It’s a strategy for sensible investors.

It’s how you give short-term spending the certainty it deserves while allowing long-term capital the opportunity to grow.

If your portfolio already has these two pots in place, a market setback should feel uncomfortable, but it shouldn’t force you to change course.

If it doesn’t, and you expect to draw income or capital within the next five years, I’d encourage you to get in touch.

We can review your arrangements together and make sure your plan is built to withstand the sort of market conditions that eventually come to every investor.

It’s far easier to put the roof on while the sun is shining than to wait until the rain arrives.